The Financial Experiment at the Foundation of the Green New Deal

The financial foundation of the Green New Deal is something called Modern Monetary Theory. I know many in our audience are excited about the Green New Deal, while many others are bewildered. This post is not about the Green New Deal, and so I’m going to ask you up front to set your feelings about it aside and focus with me instead on the financial theory at its core. And I’ll note up front here that you can be aligned with the goals of the Green New Deal without buying into Modern Monetary Theory; the two are not inseparable.

I’ve written in the past about Modern Monetary Theory, and I’ve not been shy about voicing my skepticism. A liberal-leaning friend of mine recently described it as the “Laffer Curve of the Left,” something many would like to be true because it justifies a worldview. But wishing a thing were true is not the same as it being true.

For those of you not familiar with the Laffer Curve, it was the byproduct of another economic theory—this one a product of the political right—that suggested, as one of its conclusions, that lowering tax rates would lead to increased tax revenue. As with all theories, there are data points to back the assertion, as well as internally consistent explanations for all the data points that do not.

Besides the ridiculous level of over-simplification each theory makes of complex economies, the two approaches share another characteristic: both the Laffer Curve and Modern Monetary Theory promise a financial wonder drug for those seeking to overcome financial constraints.

With the Laffer Curve, we can cut taxes and get the same revenue. With Modern Monetary Theory, we can simply create all the money we desire to spend without economic consequence. As I wrote last year:

If you discover a magic pill that is said to solve some complex and ancient problem human societies continually struggle with, you might want to pause before taking it.

I don’t want to give you a caricature of Modern Monetary Theory. Last year, I shared two lectures from individuals with very different perspectives on economic management. One of those was Stephanie Kelton, one of the leading proponents of Modern Monetary Theory. It’s important to hear an authentic representation of the approach, and I recommend you listen to her.

The Goal is Spending?

In the video below, Stephanie Kelton goes through Keynes’s Paradox of Thrift, the Depression-era insight that, while it’s rational for any one individual to save instead of spend, when we all collectively do so, it’s a disaster for the economy. This is the basis of the mainstream Keynesian economic response to recession, the idea that the government can and should spend to counteract the reduced spending in the private sector.

Modern Monetary Theory goes way beyond Keynes in this regard, but I want to linger here a moment because it’s an insight that always struck me as odd in its assumed universality. Household savings rates were very high during the post-war boom years and have been steadily declining since the mid-1970’s. We reached lows in 2006, just before the housing crisis and the beginning of the Great Recession. While the Paradox of Thrift may be applicable to the Great Depression economy (I won’t argue the point), when does thrift turn to avarice?

When have we consumed so much that we can no longer be induced to take on debt to consume more? What happens if we are satiated? As I recall my favorite economist Tomas Sedlacek saying, how do you serve a meal to someone who is full? The Paradox of Thrift does not recognize this possibility. It assumes ravenous appetites, indefinitely, and so the economy must be force fed capital—via debt—whether it has productive uses for it or not.

Kelton explains—and, again, listen to it in her own words because you need to hear it authentically from her—an economic cycle where success is measured in Gross Domestic Product (GDP). Understand that GDP is a measure of transactions. If I grow my own food and you grow your own food and we both consume what we grow, economists monitoring GDP are grumpy because there is no transaction. If I sell my food to you and you sell yours to me, transactions are created and economists are happy.

Kelton contends that capitalism runs on sales. I was always taught that capitalism runs on savings and investment (aka: capital), but let’s follow her assertions. She says that (a) capitalism runs on sales, (b) sales create income, (c) sales create jobs, ergo (d) if we want to grow the economy, we need to increase spending so there are more sales.

This narrative is baffling to me, so much so that I watched it three times to try and understand what I was missing. Sales don’t automatically create income; they only do so when the sale generates at least as much revenue as cost. Income is created when sales generate a profit, when revenues exceed expenses over the long term. In the same line of reasoning, sales don’t create jobs; profits do. I ran a planning firm with lots of sales and not many profits and, trust me, you don’t make up for losses with an increase in sales volume.

In fact, if you increase sales in unproductive transactions, you might be able to extend the life of an unproductive venture a while longer, but at tremendous damage to other parts of the economy, from investors to potential competitors to employees and suppliers. One of the theoretical features of capitalism is that it mercilessly destroys unproductive ventures. That is, unless macroeconomists interpret that destruction as recession, a Paradox of Thrift that must be overcome with government bailouts and stimulus spending.

I’m taking some pains with this because, by focusing on GDP growth, Kelton, as a leading advocate of Modern Monetary Theory, is stuck in the same macro-myopia that has been bankrupting our cities since the beginning of the post-World War II Suburban Experiment. Build a new highway and all kinds of transactions are created, but communities take on liabilities in the process and grow less and less wealthy with each transaction.

Transactions do not equal wealth creation. And for cities—and the families and small businesses within them—prosperity is about wealth creation, not transactions.

Insolvency is a Myth

One of the key “insights” of Modern Monetary Theory—and I’m going to intentionally use the obnoxious quotation marks because it’s only an insight if you ignore thousands of years of financial history—is that the United States government can never become insolvent, or become unable to pay its bills, because it has a monopoly on creating dollars. If we have debts to pay, we have the capacity to create the money needed to pay that debt.

I’ll step back and note that this insight was one of the inspirations for the creation of the Euro. Governments can use fiscal policy (deficit spending) and monetary policy (manipulation of interest rates and the quantity of money) to add or (theoretically, though rarely) subtract economic stimulus to and from their economies. Both fiscal and monetary policy have major downsides if abused, especially for the poorest and most vulnerable in society.

History demonstrates that there is far too much temptation—especially in democratic governments, but in more autocratic ones as well—to appease the masses today by borrowing, spending, and devaluing the currency in ways that create pain in the future. The Euro project is a collective recognition of this by the countries of Europe, who agreed to voluntarily give up their own monetary policy—they can’t give in to temptation because they can’t print money—and to place collective limits on fiscal policy, thus constraining the temptation to run large deficits. That is the essence of the European Union fiscal project. (I’m inserting part one of a great Tomas Sedlacek lecture on the European Project for you to come back to later.)

In contrast to the premise of the modern European Union, the Modern Monetary Theorists suggest that we need to run deficits “almost all the time.” Kelton describes “deficit hawks” as backward reactionaries ignorant of how economics works. She describes “deficit doves” in kinder terms, but still makes clear that these Keynesian thinkers are old-fashioned, at best. What Kelton supports are people she calls “deficit owls,” wise individuals who understand the contention of Modern Monetary Theory that the goal is to balance the economy and not the budget.

This is where I freak out, and I’m going to admit that freely. The theory here suggests that, in the complex adaptive system known as the U.S. economy, where hundreds of millions of individual actors make decisions each day that interact with each other in a nearly infinite variety of ways, that economists—using coarse data aggregated into spreadsheets layered in with a myriad of assumptions—can calculate the optimum GDP.

I want a pony. https://t.co/eHOMzNK0sL

— Charles Marohn (@clmarohn) February 10, 2019

And if that’s not a level of professional hubris that you find completely unwarranted by an understanding of history, my dear Icarus, know that Modern Monetary Theory suggests that the economy can be fine-tuned, through fiscal and monetary policy, by enlightened economists, so that we can achieve this optimum GDP. All we must be willing to do is spend more, especially when that means taking on more debt.

My freak out at this really comes from my inner Nassim Taleb, which finds inherent value in excess capacity. I’m going to admit (because I understand what Modern Monetary Theory is selling) that I’m not the underemployed person looking for a job, which is a less antiseptic way to describe “excess capacity” in the national economy. Even so, I don’t believe a lack of spending has caused that problem—quite the opposite, actually—nor that more spending will solve it. I think Modern Monetary Theory, when it is adopted wholesale in the U.S., is going to be most cruel to the poor.

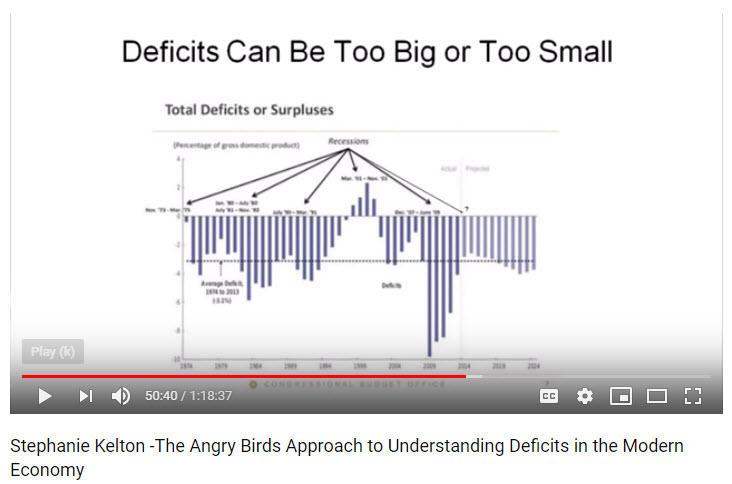

One of the most bizarre parts of Kelton’s explanation of Modern Monetary Theory comes at around the fifty-minute mark where she explains the relationship between deficit spending and recessions. According to Kelton:

“Every single time, with no exceptions, that the government deficit gets too small, we’ve had a recession. Every single time.”

What? Kelton is observing that, during a recession, tax receipts fall and government spending increases, resulting in larger deficits. She is also observing that, when the economy is not in recession, tax receipts rise and government spending normalizes. Somehow she has reversed cause and effect and construed that to mean that if we only continued to run deficits at recession levels, we would never have recessions, as if that is the goal.

As an analogy, we could plot food intake versus hunger and observe that every time food intake goes way up (because we sit down for a meal), it was preceded by an increase in hunger. If we want to avoid hunger, we should continuously consume food. That is a true statement if avoiding hunger is our one and only goal, if we’re trying to optimize the time we spend with a full stomach. Of course, that’s not our goal, and if it were, we would all become obese, sickly and underperforming. And we’d die without the feedback that hunger provides.

Hunger is as natural a part of making our bodies work as recession is to making our economy work. Only an economist, as fixated on GDP as traffic engineers fixate myopically on traffic flow, would draw such an absurd conclusion from that data.

The Unstated Assumption We Know is Wrong

One of the things that has made me a novel spokesperson for Strong Towns is that I’m an engineer who has been inside the engineering profession and found it lacking, and a planner who has been inside the planning profession and found it lacking. What is lacking is not intelligence—engineers and planners are incredibly intelligent. It’s a lack of humility that comes along with specialization.

Go to a mechanic and they will either be confident or not that they can fix your car. A car is a mechanical device that has a predictable and easily determinable set of outcomes. There is no way your mechanic tinkers with the starter and your rear wheel goes flat. It doesn’t work that way.

Economists, engineers, and planners all work in complex environments, where the systems they interact with form complex feedback loops, not only with other systems they are familiar with, but with all kinds of things they don’t even pretend to understand. I’ve spent a decade pointing out how the professional myopia of engineers and planners is making us poorer and less prosperous, sometimes even killing people. People applaud my bravery—at least, they do as long as I stick to my lane.

Suggest that economists may suffer from a similar human failing, in a realm even more opaque and disconnected from the way people live their lives, one dominated by politics and ideology, and the knives come out. I’m not applauded but branded as simple and naïve. It feels like a religion.

There is one fatal flaw in Keynesian thinking that carries over into Modern Monetary Theory which I have never heard a credible counter to, and that is the underlying assumption that the economy is sound and functioning properly but for increased government spending.

At Strong Towns, we know this is false. We know that, in our current pattern of development, the more we grow the poorer we become. We know that our cities survive based on building wealth, and more transactions does not equal more wealth, especially when those transactions result in the community taking on more long-term liabilities than revenue potential.

In the years leading up to 2008, I was telling all of the cities that my firm worked for that we were overbuilding, that we had too many lots and not enough productivity, and that this was going to end badly. When the housing market was imploding, I saw it as a long overdue correction, the unfortunate pain we had to endure for our folly. I was hopeful for the lessons to be learned.

What we got instead was the Keynesian response: prop up the housing market with TARP and Quantitative Easing, stimulus for more road building and shovel-ready projects, and money sent directly to states, cities, and schools to keep people employed. I was so bewildered I started the blog that eventually grew into the Strong Towns movement.

I don’t want people to suffer. I desperately don’t, and it pains me to watch it happen. I step back and look at what we’ve done since 2008 and acknowledge that it put off the pain for many (though far from all), but it seems to have only delayed it. And in delaying it, increased the potential severity. We’re back to building strip malls, big box stores and suburban subdivisions here in my hometown, for crying out loud! I’m scared of the unproductive economy we’ve built, and of what will happen when that lack of productivity finally bites us.

That’s under a Keynesian mindset. Now insert Modern Monetary Theory, which—according to Kelton—would have had us running even larger deficits in 2004, 2005, and 2006 when those worst imbalances were building up, revving the economy up closer to “optimum” GDP. And if things went bad, rev it up even more. I find this insane. Like, driving-off-a-cliff insane.

Around minute fifty-eight in her lecture, Kelton suggests we deficit spend in order to invest in infrastructure. She cites the American Society of Civil Engineers—an organization I’ve branded part of an “infrastructure cult”—and their demonstration of need. It’s assumed that this infrastructure spending leads to productive growth—growth in excess of the long-term liabilities we will incur. All you supporters of Modern Monetary Theory want to run a massive pass/fail experiment on American society based on that hypothesis?

I’ve said in the past that I understand why the post-war generation embarked on the Suburban Experiment. After the Great Depression and World War II, sitting on top of the world economically, with the world’s reserve currency and abundant cheap oil, it’s folly to suggest we would have done something differently. We’re all human.

Where I start to lay blame—blame which grows gradually into contempt—is the period when the bills started to come due, the decade beginning in the late 1960’s. When we felt that pain—the high inflation, increasing taxes, price controls, energy spikes, a rush on gold—we could have read that feedback as a signal that we needed a course correction, that maybe gutting our cities of wealth to provide GDP-increasing transactions wasn’t a great idea after all. Some did.

Collectively, however, we did the easier thing; we removed the painful feedback. We ended the gold-convertibility of the dollar and put the U.S. on a fiat currency. We ran huge deficits. We encouraged consolidation of financial institutions (and power) and bailed them out repeatedly, just to keep things going. We lowered interest rates and did all we could to bring future consumption into the present (anyone remember Cash for Clunkers?).

We did everything we could to avoid uncomfortable feedback. Even today, those most frantic about the impacts of climate change obsess about massive government spending programs for high speed rail and electric automobile grids instead of walkable neighborhoods and traditional downtowns. That is because their motivations start with spending on programs then move to the process of selling that spending to the masses, not the other way around.

Inflation is the Constraint?

When pushed by skeptics, proponents of Modern Monetary Theory hedge their “no constraints” rhetoric with an admission that our capacity to spend is based on inflation. If inflation gets too high, then there is too much money in circulation chasing too few resources, and there is a need to reduce spending (presumably regardless of the consequences).

We often talk about inflation merely as rising prices. If you think about that for any period of time, it becomes rather silly to think of this broad basket of goods and services aggregating into a single number, given to two decimal points no less. That single number doesn’t capture what it means for individual people’s lives. I’m 45 with two teenage girls; it doesn’t impact me if the cost of daycare is going up by 5% a year or the cost of end-of-life care is dropping by 5%, but the price of braces, tennis shoes and phones are impacting my bottom line in a big way. Yet all these things and more are brought together into a single number that is supposed to comfort us as a society or freak us all out.

When inflation was first put together as a concept, the idea was to measure what it would take to maintain a constant standard of living. If that meant a house, two cars, a television, and steak once a week, that is what was measured over time.

What economists came to realize is that, when people became poorer, they tended to substitute less-desirable goods for more-desirable. Instead of steak, you’d eat hamburger. If government bean-counters continued to assume steak, they would be over-estimating inflation rates and—perhaps more importantly in their eyes—underestimating GDP growth. In inflation calculations, making this change is called substitution.

There was also a set of realizations put forth that the quality of products changes over time, and so inflation rates began to be adjusted to account for that. None of us would want to go back to a 1980s television, for example. If we look at televisions and see that they increased in price by 10% in a given period, yet the quality improved the value by 20%, government bean-counters would conclude that the price of the television has undergone deflation. Despite the higher ticket price, it is counted as being 10% cheaper because of the added value. In inflation calculations, this is called an hedonic adjustment.

There are all kinds of things like this. For example, inflation in the house you own isn’t computed based on the value of your mortgage, it is based on market rents as if you were renting it to yourself. During our recent succession of housing bubbles—which a simple mind like mine would call a series of asset inflation episodes, one ongoing—rents did not rise as fast as prices. In fact, in most markets a home could not be rented at a rate that would cover a new mortgage. That meant the wild house price inflations were tremendously understated in official inflation calculations.

None of this is nefarious—it’s all done out in the open—but it’s not well known that published inflation rates assume you’re renting your own house at lower rates than what you’re paying, eating hamburger instead of steak because you’re poorer, and watching a $50 television that cost you $900 in cash but had $850 in hedonically-adjusted value.

So, if inflation is the only constraint with Modern Monetary Theory, it makes a lot of difference how it is calculated.

There is a site maintained by stat geek John Williams called ShadowStats that reports on government statistics. Warning: It’s one of those sites that is frequently consulted by people in business and finance, but because it questions government statistics, it’s not frequently cited by those overseen by regulators. Modern Monetary Theory proponents don’t like it, to the point of sneering at it, so take that for what it’s worth. For me, it’s important to understand that there is an alternate narrative on inflation that I find has some level of credibility.

Here’s how Shadowstats describes changes to the inflation rate:

In the early-1990s, political Washington moved to change the nature of the CPI [Consumer Price Index]. The contention was that the CPI overstated inflation. Both sides of the aisle and the financial media touted the benefits of a “more-accurate” CPI, one that would allow the substitution of goods and services.

The plan was to reduce cost of living adjustments for government payments to Social Security recipients, etc. The cuts in reported inflation were an effort to reduce the federal deficit without anyone in Congress having to do the politically impossible: to vote against Social Security. The inflation-calculation changes had the further benefit to government fiscal conditions of pushing taxpayers artificially into higher tax brackets, thus increasing tax revenues. The changes afoot were publicized, albeit under the cover of academic theories. Few in the public paid any attention.

The site goes on to include some more salacious details that don’t make politicians look very good, but it doesn’t matter. Good people honestly felt this was the right thing to do, and maybe it was. Maybe this is the right way to calculate inflation and GDP growth, or maybe it’s just the most convenient way to remove constraints. It’s hard to tell.

Now step back and imagine for a moment the political leader you hate the most, the one you implicitly distrust and believe is only out for their own gain. Put that person in one of the three top leadership positions in our centralized economy—President, Speaker of the House, Federal Reserve Chair—and imagine these words being uttered to the commissioner of the Bureau of Labor Statistics as they ponder how to substitute and hedonically adjust for the next round of inflation reporting:

“If you could see your way clear to doing these things, we might have more money for BLS programs.”

Click on the chart to click through to Shadowstats.com.

These things, of course, being a favorable number. The stakes are high, after all, and at many forks in the road there are two plausible paths. We’re human, so human. Even economists.

I take no comfort in government-reported inflation rates as a constraint on government-desired spending. By the way, Shadowstats suggests that the real inflation rate—the rate that prices are going up to maintain a set standard of living—is close to 10%, quite a bit higher than the government’s reported rate of less than 2%.

A Barbarous Relic

Modern Monetary Theorists hold particular disdain for gold-backing of the currency. At the end of World War II, the United States brokered the Bretton Woods agreement that established the U.S. Dollar as the world’s reserve currency. The dollar was backed by gold and fully convertible; any country with $35 could show up and demand an ounce of gold from the Federal Reserve. This made the dollar as good as gold, which was important for trust in the post-war rebuilding.

That trust went away when the United States abused the privilege of a reserve currency and printed far more dollars than the economy could absorb. This devaluation of the currency meant that, in real terms, it should take much more than $35 to buy an ounce of gold. When the French showed up in 1971 with a pile of cash demanding gold, President Nixon temporarily closed the gold window until financial order could be re-established. It’s never been reopened.

Economists like Kelton point to this as a turning point in a process of liberation. In her talk, she laments a lingering pre-1971 mindset, the notion that our spending is constrained by antiquated notions from the days when gold-backing was a constraint.

Thomas Piketty is the author of Capital in the Twenty-first Century, a book that details rising income and wealth inequality that occurred in the last century. I read it; it was a fascinating book, although I was continually struck by the changes that happen on many measurements of inequality starting in the 1970’s. Check out this story in the New Yorker that details Piketty’s inequality story in six charts, and see what I mean.

With these charts of rising inequality in mind, and with an understanding of how the constraints of gold removed in the early 1970’s, and inflation reporting was loosened up over the subsequent decades, ponder this insight from John Maynard Keynes from his book The Economic Consequences of Peace:

Lenin is said to have declared that the best way to destroy the capitalist system was to debauch the currency. By a continuing process of inflation, governments can confiscate, secretly and unobserved, an important part of the wealth of their citizens. By this method they not only confiscate, but they confiscate arbitrarily; and, while the process impoverishes many, it actually enriches some. The sight of this arbitrary rearrangement of riches strikes not only at security but [also] at confidence in the equity of the existing distribution of wealth.

Those to whom the system brings windfalls, beyond their deserts and even beyond their expectations or desires, become "profiteers," who are the object of the hatred of the bourgeoisie, whom the inflationism has impoverished, not less than of the proletariat. As the inflation proceeds and the real value of the currency fluctuates wildly from month to month, all permanent relations between debtors and creditors, which form the ultimate foundation of capitalism, become so utterly disordered as to be almost meaningless; and the process of wealth-getting degenerates into a gamble and a lottery.

Lenin was certainly right. There is no subtler, no surer means of overturning the existing basis of society than to debauch the currency. The process engages all the hidden forces of economic law on the side of destruction, and does it in a manner which not one man in a million is able to diagnose.

A process that impoverishes many, enriches some, through an arbitrary rearrangement of riches. Why is it considered enlightened to want to turn financial stewardship of the country—and to some extent, the world—over to transaction-obsessed economists pushing a convenient theory in league with politicians and corporations that stand to directly benefit from its application? And why is it dismissed as antiquated and barbaric to seek a hard constraint on our profligacy?

I don’t want my economy—or my life—optimized by Modern Monetary theorists, regardless of the good they think they can accomplish as a result.

Modern Monetary Theory is Coming, Regardless

We have serious, difficult choices to make on a wide range of critical issues. I’ve not run from those. Strong Towns is trying to take on what is perhaps the biggest: the massive experiment in rearranging our human habitat that we embarked on after World War II. We do not shy away from bold action.

Modern Monetary Theory pretends to be a courageous alternative. It is the opposite: a way to sell a series of programs to the masses based on an understanding that the pain will only come to a select few bad people. There is no shared sacrifice. There is no mutual responsibility. In this new world of Modern Monetary Theory, we owe each other nothing but the courage to trust those who would optimize things on our behalf.

It doesn’t matter. I’m convinced we’re going to get Modern Monetary Theory whether we want it or not. Republicans have demonstrated over the past two years—as if we needed more proof—that their rhetoric on fiscal restraint will never be matched by deeds, that deficits do not matter to the so-called conservative party. As candidates for president line up on the Democratic side, there is universal support for the Green New Deal and, ostensibly, the easy financial choice resting at its optimistic foundation.

The financial website Epsilon Theory has a great article on Modern Monetary Theory, a play on the classic Dr. Strangelove, titled How I Learned to Stop Worrying and Love the National Debt. The story made this observation:

MMT is the post hoc justification of both easy fiscal policy and easy monetary policy. As such, it is the new intellectual darling of every political and market Missionary of the Left AND the Right.

MMT is the theoretical justification for the economic policies of Trump and his Wall Street fellow travelers alike, who want nothing more than to keep the market punchbowl in place and well-spiked with pure grain ZIRP alcohol forever and ever, amen.

MMT is the theoretical justification for the economic policies of every potential Democratic presidential candidate in 2020. Because with MMT, you CAN have it all. You can pay for wars without end. You can pay for universal single-payer healthcare. You can pay for everyone to go to college. You can pay for a universal basic income. I mean … why not? A caring sovereign’s gotta do what a caring sovereign’s gotta do.

Modern Monetary Theory is going to be a disaster for our cities. Yes, we’ll pump a bunch of money into fixing up frontage roads and factory school campuses. Maybe we’ll “rebuild every building” and, in the process, put solar panels on that big-box store or hook up those suburban McMansions to a wind farm. We can build some new rail lines and get some condos out there, the kind with a few affordable units on the back side. We’ll make it rain and it will all be good.

Until it’s not, and that’s when cities, and the people who live in them, will find out that they are utterly on their own, tasked with doing the impossible —maintaining this broad expanse of American wasteland we have constructed—without anywhere near the wealth needed to make it happen. It is then that the last of us will stop measuring success in terms of transactions, stop being beholden to forces outside our control, and start recognizing the value in each other and what we can do together.

We need to start building Strong Towns. We need to get going now.

Charles Marohn (known as “Chuck” to friends and colleagues) is the founder and president of Strong Towns and the bestselling author of “Escaping the Housing Trap: The Strong Towns Response to the Housing Crisis.” With decades of experience as a land use planner and civil engineer, Marohn is on a mission to help cities and towns become stronger and more prosperous. He spreads the Strong Towns message through in-person presentations, the Strong Towns Podcast, and his books and articles. In recognition of his efforts and impact, Planetizen named him one of the 15 Most Influential Urbanists of all time in 2017 and 2023.