Fixing Finance for Small-Scale Development

This article is part four in a five-part series on small-scale, incremental development. You can read part three here, and sign up here to receive the e-book for this series when it’s available.

A net zero home project in South Bend, IN, by small-scale developer Mike Keen, in collaboration with Habitat for Humanity.

At the root of any ecosystem you’ll find a food chain. Start with the question of what resources are available (i.e., sunlight, water, nitrogen and other nutrients). Everything else, while not entirely determined by that, ultimately has to follow from it.

For development, finance is fertilizer. Most of the developers I spoke with cited access to capital as a significant barrier to the kinds of small infill projects they would like to do—and even more so, to creating more small developers doing more projects.

This isn’t because the money isn’t there to be had. At any given time there is more money looking for a good project to invest in than vice versa. But development in North America has a “Who” and a “What” problem.

What gets built today? Mostly formulaic buildings adhering to one of several fairly predictable templates: the monoculture crops of the suburban experiment.

Who builds it? Mostly large to very large development firms. Rarely the people with the most skin in the game: those who live in the neighborhoods they will be developing.

Each of these dilemmas has different answers depending on the scale at which you examine it. It’s important to understand the barriers facing, and options available to, an individual developer. But it’s also important to interrogate the systems that constrain those options in the first place, and to look at what role higher levels of government might play in removing some sources of distortion, and thus freeing up opportunities for individuals to generate wealth for their communities.

The “Who”: What Does it Mean to Be Bankable?

There’s a huge amount of ingenuity and energy in struggling neighborhoods among people who would love to contribute to their renaissance, but it takes outside support to channel that energy into development. In addition to bank loans, small developers typically work with investor partners who contribute equity up front to the project. At the small scale, this is likely to be someone you know and have a personal relationship with.

This is where building a conscious community centered around incremental development, not just a bunch of go-it-alone entrepreneurs, can be transformative. It’s incumbent on those who already have social and institutional capital to help make it so that you don’t have to be independently wealthy—or already have a friend who is—in order to get started in development.

Jenifer Acosta.

Jenifer Acosta of Bay City, Michigan, does historic renovation and adaptive reuse projects, both residential and commercial. She is keenly aware of the access she has, and tries to pay it forward. “It was only 50 years ago that a bank could have denied me a loan as a woman, because the Equal Credit Act wasn’t passed yet. Cities shouldn’t be built by the same 10 white guys.” Acosta serves on her community foundation’s impact investment committee, and does development consulting locally as well as serving on the faculty of the Incremental Development Alliance—always looking to bring others up with her and help others make the connections they need.

“Access is a big deal in a small town, and poverty is a big deal,” Acosta says. “We’ve spent so long telling people that they don’t necessarily belong in this world. How do you make people bankable? A colleague develops 30 minutes from my house; I’ve known him five years and did his technical assistance, since I knew the local players.”

When you come from a background of poverty, it’s easy to feel almost traumatized by the experience of trying to deal with financial institutions, and to feel like you cannot advocate for your own self-worth through your life experience, Acosta says. But these are the developers we need. “It’d be faster for me to be like, ‘Hey, I’ve got your backing.’ But I teach people how to advocate for themselves, bring in that investor capital and not be ashamed of it. It’s just money, right? Money needs to do some sort of purpose.”

Derek Avery is a developer in Dallas, Texas, who sees his work building affordable market-rate homes (and, more recently, office space) in neglected neighborhoods as mission-oriented “revitalization without gentrification.” (You can find prior Strong Towns interviews with Avery here and here.) Avery is generous with advice and support for others who want to do the work, but he doesn’t sugar-coat the difficulties involved. When I asked him what it would take to create 10 times as many Derek Averys, he said, “I like to talk about wins and losses with this, so that it’s real. I’ve been able to successfully complete projects, but it’s hit and miss if they’re profitable. I have had more projects that are not profitable than are. [Small-scale development] still takes capital that most people don’t have, and it takes risk that most people aren’t in the position to take on.”

Derek Avery speaking at a Strong Towns gathering in Plano, Texas in 2018.

This risk doesn’t end once you do your first successful project. Even experienced developers who can get a construction loan are going to have funding gaps, particularly when working in challenging neighborhoods. For Avery, a reliable line of credit allowing for cash flow throughout a project is high on his wish list. “Not everyone can cash out the 401k or borrow from friends and family,” he says. “I put every dime I’ve ever saved into it. I was using my own personal money, putting risk on my family. That’s the stress you don’t need. I’ve had failures that could have been stopped if I had access to capital that wasn’t dependent on me having so much collateral.”

This access means gap financing: finding ways to help small developers cover the difference between what a bank loan will pay (often 70%) and the actual cost of a project, without dipping into their personal assets and risking ruin. Governments and nonprofits can be difference-makers here, helping to scale up the principle of bringing someone along and making them bankable beyond personal relationships.

One idea the Incremental Development Alliance (IDA) has explored is finding a way to guarantee loans or a better interest rate linked to participation in the IDA’s boot camp programs. This might involve non-traditional sources of finance, whether impact investing or working with community development financial institutions (CDFIs).

Fixing the Focus of Economic Development Programs

Local governments aren’t investors, but they can lend their own creditworthiness, not by giving away scarce public dollars but by backstopping affordable gap financing, and offering it to small developers through a revolving loan fund. In South Bend, the Economic Empowerment department has discussed whether, partnering with a local bank, the city could chip in to buy down the interest rate, giving developers access to a 2% loan instead of 5% or 8%.

Government-backed loan programs can fall into the trap of having conditions that are too rigid to be useful. For example, a revolving loan fund that already exists in South Bend, with some state funding, is set up for single-entity businesses, but not mixed-use projects. This makes it useless for, say, South Bend developer Maricela Navarro, who is renovating a historic building to contain space for four businesses, two apartments, and four storage units.

While existing programs for the smallest developers don’t serve many use cases, local governments have a long history of making capital available to large developers in ways that small ones can’t access, such as Tax Increment Financing deals. Simply redirecting conventional economic development resources—tax incentives, pass-through block grants, and one-time things like COVID stimulus money when they come—to supporting small developers could be transformative.

Alkeyna Aldridge, South Bend’s Director of Engagement and Economic Empowerment, describes herself as “a nuisance to my peers, because I’m pushing them to ask questions they haven’t asked. Like how do we take care of the folks we have, and create mobility for new Americans in our community? In the way they’ve been trained, [incremental development] is not a growth model. I’ll be asked things like, ‘Why are you focusing on folks who are not ready to do development?’”

The proof is in the results, though. Incremental development, if anything, creates more enduring value than large-scale projects.

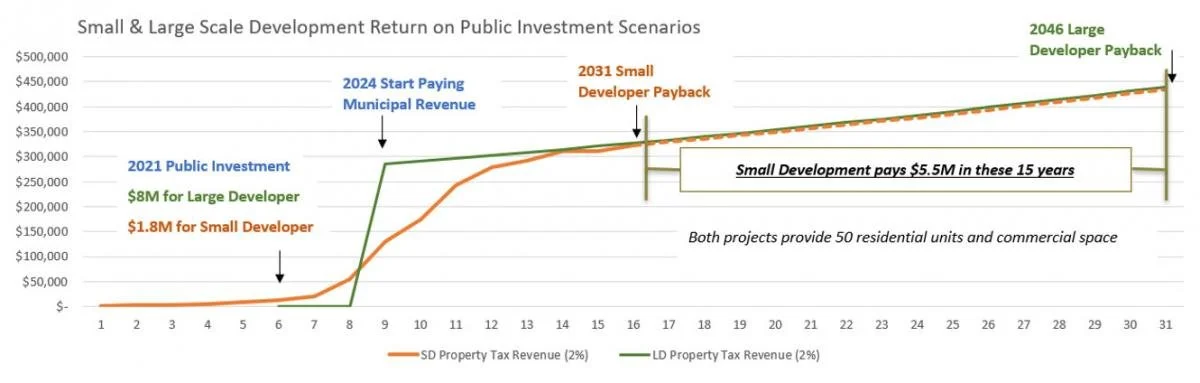

The case study of Mike Keen’s Portage Midtown ”farm” in South Bend (discussed in the previous installment of this series) is merely one illustration. A financial analysis by Neil Heller of Neighborhood Workshop estimated that by 2031, redevelopment of these 95 small lots over only three acres would produce $15.2 million in private investment, while generating 50 new homes and 172 jobs. But Heller also contrasted this performance to a hypothetical scenario in which a single large building were built containing the same amount of housing and commercial space. Under that scenario, $8 million in up-front tax incentives would be necessary to render the project viable in South Bend’s market. As a result, the large development wouldn’t pay off its public investment until 2046: fifteen years later than the incremental approach. (In fact, Heller writes, Keen and his partners were able to acquire the Ward Bakery building “after acquiring mid-size developers joined the ranks of six previous failed attempts at a New Markets Tax Credit application. Mike’s ‘farmers’ have created enough value that tax credits are not needed.”)

Image via Neil Heller.

In the real world, the comparison is even starker, because Heller assumed an equivalent level of development intensity for the sake of argument. But in practice, a granular pattern of small lots almost always uses land more intensively, and with more attention to wringing value out of the space, than a large development in the same market context, resulting in the stark contrasts Strong Towns has documented for years. The most financially productive land users in our cities are often small businesses on the most modest of lots: the Jimmy’s Pizzas of the world.

Thus, although there is a moral, fairness component to the question of, “Who develops our cities?” the problem or the solution need not even be framed in moral terms. The financial logic—behind thickening up neighborhoods already served by infrastructure, bringing life back to old buildings in places like South Bend, and getting energy and talent off the sidelines by allowing people in low-wealth communities to participate in this process—is rock-solid.

The Davidson, a historic rehabilitation completed by Jenifer Acosta in downtown Bay City, MI.

The “What”: the Monoculture Chicken-Egg Problem

There are a handful of standard loan products that offer low interest rates, preferential terms, and a straightforward, streamlined process to qualify. These tend to exclude the kinds of projects that many incremental developers want to do—urban infill buildings that are often mixed use, usually rental properties, and often denser and with less parking than has been the norm for the last 70 years.

A key reason is the lack of a secondary market in such loans. The secondary markets are where banks resell loans they have issued to third parties. There is a massive secondary market for home mortgages, dominated by Fannie Mae and Freddie Mac, which buy home mortgages and bundle them into mortgage-backed securities. There is no equivalent for mixed-use loans. A report called “The Unintended Consequences of Housing Finance,” published in 2016 by the Regional Plan Association, explains the significance of this fact:

In practice these projects would be good investments, but require time and openness from the lender, and an interest in supporting the local community. Yet as there is no secondary market for mixed use loans, they are held on the bank’s balance sheets, keeping the bank from “reusing” the funds for other loans and collecting more fees. Including these opportunity costs, the loans are notably more expensive for the bank, and thus expensive to the developer. Banks prefer “cookie cutter” conforming loans and sell them easily, but non-conforming loans are relatively rare, expensive, and unsalable. Generally the loans simply are not made, and without financing opportunities many mixed use projects, especially in older areas, aren’t conceived.

How did it get this way? One interpretation, offered by Stephen Smith, is that “finance issues are actually zoning issues.” Because land-use regulation restricts the vast majority of urban land in the U.S. to single-use structures, and in the case of residential areas, typically 80% or more to single-family homes, banks don’t find it worthwhile to create loan products for building types that are uncommon.

On some level, though, the problem is almost certainly a chicken-egg one. At times, it’s lenders, not regulators, restricting development practices. Accessory dwelling units (ADUs) are often poorly served by existing loan products, even in cities where they are allowed and encouraged by the planning department. And for commercial buildings, it’s not uncommon that a loan officer will insist on more parking than the zoning itself requires. Banks have acquired their own ideas about what is high or low-risk in development.

These ideas may have little empirical grounding, but they have a long history. Many date to the Federal Housing Administration’s original sin, in the 1930s, of defining mixed-use buildings and apartments, and urban areas with many of them, as “hazardous” for the purpose of insuring loans, a key component of mortgage redlining. This belief was baseless at the time, let alone now, yet its legacy is still present in our banking system.

There is some momentum for federal reform. 2016 changes to FHA loan guidelines allowed up to 49% of a property to be commercial, up from the previous 25%. More work needs to be done to democratize these standard, easy-to-access loan products, though. One low-hanging possibility is to adjust the 203(K) program, which provides a loan for rehabilitation of a home that then becomes a conventional mortgage, to more easily finance the construction of ADUs, by letting borrowers borrow against the future rental income stream from the ADU. Combined with Kronberg’s suggested policy of allowing fee-simple ADUs (essentially dividing a residential lot in two), there would be a straightforward source of financing to take virtually any single-family home to the next increment of development: two homes.

Two Paths for Developers: Form Follows Finance, or Find a Better Bank (If You Can)

From the perspective of an individual developer, you can’t do much to fix the system, but you can work within it in one of two ways.

One is to embrace the principle of “Form Follows Finance,” a catch phrase I learned from the Incremental Development Alliance. This is another way of saying what Eric Kronberg told me: “Feed the lenders and appraisers what they eat.”

For a small developer, there are a few templates that fit within the strictures of well-established loan products—if your situation and goals are compatible. One is a standard FHA loan which converts to a federally-insured 30-year mortgage upon completion of the building. You can use this on a house of up to four units, as long as one of them is your primary residence. Up to 49% of the building can also be commercial space, but a number of other issues surrounding appraisal can still present roadblocks. Another option, pointed out to me by Monte Anderson, is a Small Business Administration (SBA) loan, which can cover the construction of a building in which your business occupies at least 60% of the space. The remaining 40% can be turned into rental apartments providing an income stream.

The other path is to find a lender who “gets” it and build a good working relationship with them. Here, local banks and CDFIs shine. This has been a big part of the story in South Bend’s small developer ecosystem. I spoke with Gary Benedix of Northwest Bank, which has been a key factor in that ecosystem. Benedix told me it’s common for individual banks to specialize in certain kinds of loans or refrain from others. In the case of Northwest, the small business program is particularly flexible, and the bank has a longstanding commitment to working with neighborhoods to promote local investment.

Benedix’s biography, in some ways, illustrates why he is the exception rather than the rule. “I worked my way through college as a county commissioner up in Michigan,” he told me, “and the liaison to the regional economic development commission, so I learned things through osmosis. My senior VP was the director of a downtown development corporation in Buffalo.” Northwest Bank has sponsored a local arts fair, and talked with the Near Northwest Neighborhood about a revolving loan fund to help home renovators overcome appraisal gaps.

The knowledge required to evaluate the strength of a small development opportunity is often hyper local. It includes not just the usual factors like the presence of experienced developers on the team and an investor backer with some collateral, but also things like the relationship the developers have with the city and the neighborhood, and context about other in-progress efforts that might affect that neighborhood’s trajectory. (This is the whole “farm” concept again.)

This is one of many reasons that consolidation in the U.S. banking sector is a worrisome long-term trend; very often it takes a local bank to even entertain working with a small local developer. It will be very difficult to scale up the number of lenders who “get it,” and thus small developers who get the loans they need, without robust local banks.

Even with the Gary Benedixes of the world playing a vital role, educating bankers about community development is hardly a comprehensive answer to the system’s tilt in favor of large enterprises and standardized development products. Reform at that broader, systemic scale—likely starting with the FHA, Fannie, and Freddie, is beyond the scope of this essay or my expertise, but it starts with recognizing the role that federal mortgage policy and the derivatives market have played in putting a very, very heavy thumb on the scale.

The IDA’s Monte Anderson has a plea: for federal changes that would allow for more flexible terms on smaller loans—under, say, $2 million. “I’m not saying no regulation. But it’s very rigid right now. If you want to build a mixed-use building, it’s 30% down.”

“It’s a double whammy on small developers: financing is strict, the code doesn’t work, and you can’t get any of the incentives that you get as a big developer. Cities create these complicated capital stacks and tax credit nightmares that cause odd things to be upon the earth. All we’re asking for is cheap equity and cheap finance.”

Read part five of this series here, or click below to get a free copy of the full series in e-book form!

Who is actually going to do the work of incremental development, and what will their motivations be?